Information on the GRI standards

I. Reporting Practice

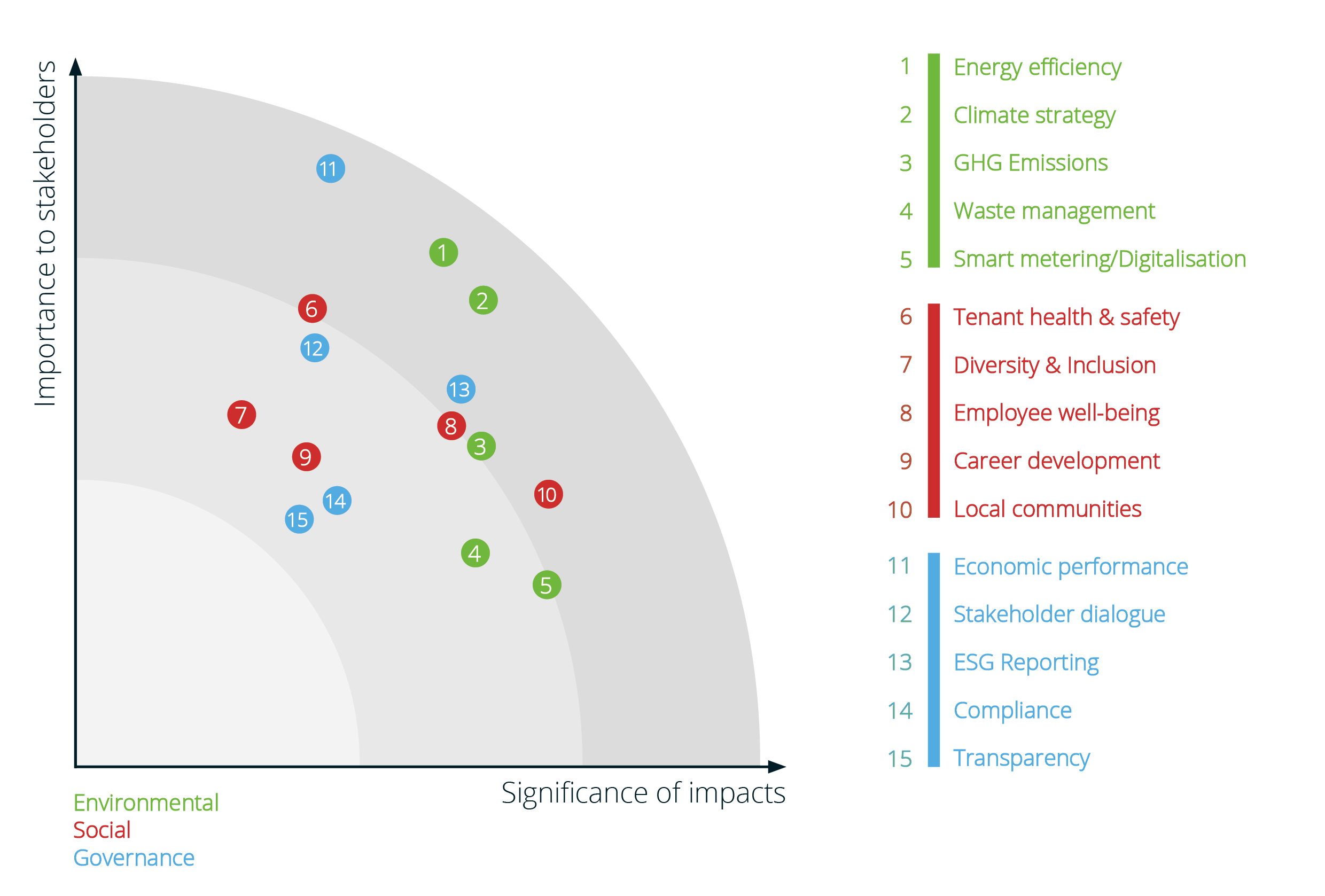

The ESG Report 2020 refers to the calendar year 2019. The developments in the areas E, S and G illustrate the annual comparison of 2018 to 2019. If certain events and information are relevant for reporting, they are also presented up to the editorial deadline of 31 July 2020. We report in accordance with the GRI standards (“core” option) and have prepared a corresponding materiality analysis. It ensures that all topics that are important to our stakeholders are addressed in this report.

Our key stakeholder groups include our customers, employees, investors and tenants. To integrate their assessments in a meaningful way, our Group Sustainability Office listed potentially important sustainability topics in spring 2020 and asked the responsible persons for the respective stakeholder group to prioritise the topics.

Our sustainability report is digital – and with good reason. More than two kilos of wood are needed for one kilo of paper, and we wish to reduce our environmental impact this year. Besides, we can provide you with broad information on our ESG topics through numerous video interviews and animated graphics. We are offering an accompanying brochure that summarises the developments, challenges and outlook on ESG at CORESTATE.

II. Materiality analysis

In the materiality analysis, companies not only ascertain the relevance of a sustainability topic from the perspective of the stakeholders but also evaluate the effects of their activities.

Determination of the relevance of a sustainability topic from a stakeholder perspective: The Group Sustainability Office has listed all relevant sustainability issues in detail and presented them to senior staff from the Human Resources, Asset Management, Client Relations and Investor Relations departments. These employees have selected and prioritised the most important topics for their respective target groups – employees, tenants, customers and investors. The resulting cluster of topics represents what is considered critical to stakeholders.

Effects of entrepreneurial activity (impact assessment):

Less direct is the so-called impact assessment. It measures the effects of entrepreneurial activity. To date, there are no standardised, manageable methods for this. Studies on the impact of the real estate sector on the environment and society were used to find out which corporate activities have a significant effect on the economic, social and ecological environment.

The resulting materiality matrix was presented to and approved by the ESG Committee, including the CEO and CIO, in May 2020. The ESG report 2020 systematically covers the topics identified.

| Topics | GRI standards |

|---|---|

| Energy for new construction, conversion, existing buildings Emissions from new construction, conversion, existing buildings Waste management for new construction, conversion, existing buildings Climate strategy for new construction, conversion, existing buildings |

GRI 302 Energy GRI 305 Emissions GRI 306 Waste |

| Corporate culture and work-life balance Training and further education of employees Diversity within the company Impact on local communities Tenant satisfaction, safety & health |

GRI 403 Occupational Health and Safety GRI 404 Training and Education GRI 405 Diversity and equal opportunities GRI 413 Local communities |

| Long-term economic stability Transparency & Stakeholder Dialogue ESG reporting Compliance |

GRI 201 Economic performance GRI 102-40 – 102-43 Stakeholder engagement GRI 102-45 – 102-56 Reporting Practice |