The COVID-19 pandemic is the most impactful social, cultural and economic event in more than fifty years. Forecasts in this environment are highly difficult and complex. Because of the many unknowns, the chain of causality becomes less predictable the further one goes down the stream. To be precise: what happens to the real estate market depends on the development of the economy, which depends on the further development of the pandemic itself. And there are still many unknowns.

However, given that the SARS-CoV-2 virus has only been known for a little longer than six months, it is remarkable what we do already know and how quickly we accumulate knowledge. In fact, it is likely that this will be the fastest turnaround time for the development of a vaccine against a new

disease in human history.

This article will provide the key knowns and unknowns as of mid-May 2020 for the virus and the economy and provide a high-level perspective what this means for real estate markets.

The Virus1

Knowns

The SARS-CoV-2 virus is believed to have spread out of Wuhan, China, around the world and the WHO has declared it a pandemic on March 12th . The USA, Europe and China have so far been the regions that were mostly hit, while more recently, the confirmed cases in emerging markets rose. COVID-19 is a highly contagious disease, which has a high fatality rate among the elderly and persons with pre-conditions. It is less of a threat for younger and healthy persons. While the situation differs regionally, from a global and general perspective, the curve is flattening, meaning that the number of new cases declines.

At the beginning of May 2020, research was conducted concerning 90 different vaccines2 and WHO’s Director General Tedros Adhanom Ghebreyesus stated that about seven to eight are promising.

Exhibit 1: Cumulative confirmed COVID-19 cases

Unknowns

When – and if – a vaccine is developed and released to the market, however, remains unknown. A vaccine, though, is crucial to fostering a normalisation of social life and economic activity.

The other major unknown is whether antibodies to SARS-CoV-2 are developed after infection with the virus and induce immunity. What is typically the case with similar viruses has yet to be proven by medical research.

Lastly, while data on COVID-19 is good, there also is supposed to be a high number of shadow-cases of the disease. These factors make precise forecasts on the further development of COVID-19 extremely difficult.

The society and the economy

Knowns

In mid-May, 65% of the world3 have been under some form of lock-down and international travel is highly restricted. While many countries in Europe have just started or are preparing to begin relaxation of the measures, in China the development is about two months ahead. It can therefore function as a proxy as to how an easing of safety and lock-down measures will affect economic activity.

It is certain that we are in the middle of a rare global recession4 and it becomes increasingly obvious that Europe’s economic decline will be more pronounced than during 2008/09’s GFC recession. The short-term impact on the labour market is unprecedented around the globe. While often mitigated by partial activity schemes, unemployment rates and unemployment claims have shot up at alarming rates.

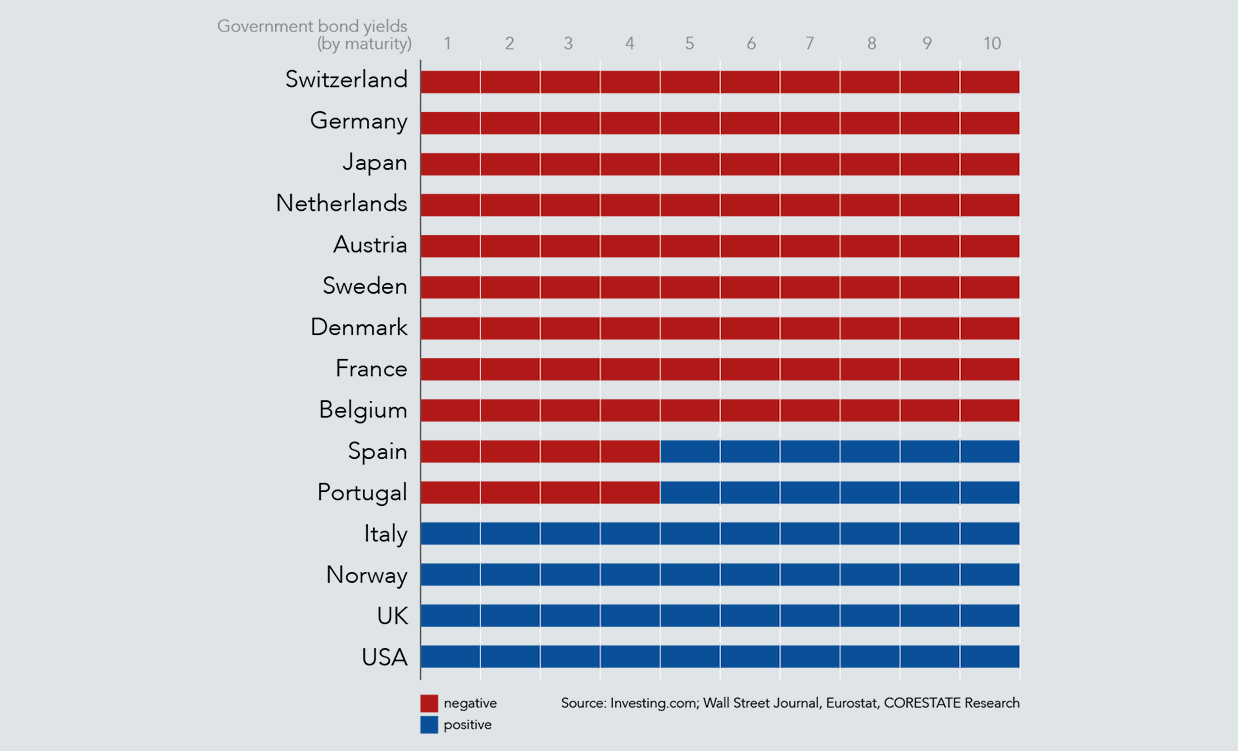

Exhibit 2: Government bond yields by maturity

To support the economy and labour markets, governments implement stimulus packages5 that range from tax reliefs over insolvency protection to direct checks – helicopter money. The consequence of these measures will be more public debt.

Central banks have become very accommodative very quickly. As a result of this and the overall market uncertainty, government bond yields for countries seen as safe have plummeted to all-time low levels.

Oxford Economics expects German 10-year government bond yields to return back to positive territory not earlier than 2022. In this ‘even-lower-for-even-longer’ interest rate environment, higher yielding asset classes, like real estate, are likely to see strong investor demand.

Unknowns

What remains unknown is the exact outcome of the economic decline and the recovery thereafter. The bandwidth of forecast GDP declines for 2020 is wider than ever and so are predictions for the economic recovery in 2021. What also remains subject to many discussions is the shape and the length of the cycle. Is it a ‘V’, a ‘U’, an ‘L’ or somewhat more creative like a Nike ‘Swoosh’ ![]() or a ‘tick box symbol’

or a ‘tick box symbol’ ![]() .

.

We believe the latter shape is the most likely form of the cycle. The deep slump during the recession will be followed by a strong initial bounce back that will then slow. It is likely that the deep recession will leave some scars and it will take time before manufacturing order books are filling up and before tourism returns to normal. Given the impact on the labour markets, it is also likely that consumers will turn more cautious and savings ratios rise.

Where does this leave real estate?

At a very macro level, the effects of the COVID-19 pandemic will mostly concern the income (rental) side of the real estate market, while the yield side should remain relatively defensive – supported by the low interest rate environment, which will support investor demand for property.

The income side strongly depends on economic activity and is complex and heterogenous among property sectors and geographies.

While residential, with its high diversity of tenants and relative inelasticity of demand, is likely to be the least affected in the current environment, impacts on the retail, hotel and leisure side are direct and deep. The logistics and even more so the office markets are sort of a mixed bag and strongly depend on the individual tenancy and industry the covenant is in. While co-working, for example, is directly hit and will likely see longer-term impacts, ecommerce operators and public sector tenants should prove resilient.

This PropBlog will analyse individual sectors over time as the situation progresses. For a first glimpse on individual sectors and how we handle the situation from an operational standpoint, please have a look at CORESTATE’s Investor Communication document.

On the investment side, which is highly impacted by the interest rate situation, particularly the core end of the market should remain a stable asset during the downturn. Core meaning specifically security of income, which is quality and length of the tenancy. Over the very short-term, though, COVID-19 will have a profound effect on transaction activity for two reasons:

a) for practical reasons: it is difficult to do site visits, for example

b) for economical reasons: given the high uncertainty that we are still in, as explained above, investors are more cautious at the moment but monitor the market closely.

Once the unknowns disappear and risks are easier to quantify, we expect market activity to return. Already now, investors are looking for opportunities to invest in. And as the situation progresses, we believe that market opportunities will arise. Here, selectiveness and a balanced approach between cyclical and long-term factors are key for successful investments.

1All COVID-19 related data is as of May 18 th 2020, unless otherwise stated | 2 Nature, vol 580 | 3 In terms of global GDP, source: Oxford Economics | 4 After WW2, there were four global recessions (1975, 1982, 1991 and 2009); source: IMF | 5 The USA alone have implemented a USD 2.3trn Coronavirus Aid, Relief and Economy Security Act. For a list of all measures, visit the IMF https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19

DISCLAIMER

This document has been prepared for general information purposes only. It does not constitute an offer or invitation to sell or issue, or to purchase or subscribe any shares in funds, securities or financial instruments, or any other shareholdings in or distributed by CORESTATE Capital Holding S.A. or any other company of the CORESTATE Capital Group (hereafter collectively referred to as the “Company”). No part of this document nor the fact of its distribution be or form part of or be relied on in connection with any contract or investment decision relating thereto, nor does it constitute a recommendation regarding the securities or the shares in funds or other financial instruments of the Company or of another entity. Therefore, this cannot be deemed as financial services, investment advisory services, an offer for the acquisition of a financial instrument or general investment advice, legal or tax advice.

The data and information contained herein has been obtained from various sources is believed to be reliable and accurate. All data and information derive from sources which the Company believes to be reliable. Furthermore, the Company has used its best endeavors to ensure that the presented facts and opinions are adequate and correct. Forward-looking statements and statements are based on current estimates, expectations and forecasts of the Company regarding market and industry developments at the time of preparation.

Nevertheless, no reliance may be placed for any purposes on the information contained in this document or on its completeness, accuracy or fairness. Neither the Company nor any of its directors, officers or employees or any other person makes any warranty or gives any guarantee, neither express nor implied, as to the accuracy or completeness of the information contained in this document, and accepts no liability for loss or damage of any kind in connection with this document, unless caused by gross negligence or intent of the Company and unless standing in a causal connection to the potential damage. The information is subject to change at any time (even without notification to the recipients). This document is an advertisement and not a financial analysis or a prospectus. The information and opinions expressed in this document are provided as of the date of this document. Certain statements, beliefs and opinions in this document, are forward-looking, which reflect the Company’s or, as appropriate, the Company’s directors’ current expectations and projections about future events. By their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that could cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and assumptions could adversely affect the outcome and financial effects of the plans and events described herein. Forward-looking statements contained in this document regarding past trends or activities should not be taken as a representation that such trends or activities will continue in the future. The Company does not undertake any obligation to update or revise any forward-looking statements. You should not place undue reliance on forward-looking statements, which speak only as of the date of this document. No statement in this presentation is intended to be nor may it be construed to be a profit forecast. By attending the presentation to which this document relates or by accepting a copy of this document you agree to be bound by the foregoing limitations and, in particular that you have read and agreed to comply with the contents of this notice.

This presentation has been compiled by Corestate Capital Investors (Europe) GmbH, a company of the CORESTATE Capital Group, 19.05.2020.